SaaS M&A hit a record high in 2025. 2,698 SaaS transactions closed over the course of the year, a 28% increase from 2024 and the highest annual total ever recorded. Private equity buyers participated in nearly 58% of all deals, and the global SaaS market is forecast to reach $465 billion in 2026. That momentum is not slowing down. With PE dry powder sitting at $3.7 trillion globally and interest rates moderating, 2026 is shaping up to be one of the most active years for SaaS acquisitions on record.

But opportunity and risk run in parallel. A SaaS business with clean recurring revenue, low churn, and a defensible product can be a wealth-building asset. One with hidden technical debt, inflated metrics, or customer concentration problems can drain capital faster than you anticipated. The difference between a great acquisition and a costly mistake almost always comes down to due diligence.

This guide is built for buyers. Whether you are a first-time acquirer, a serial entrepreneur, or a PE firm evaluating your next platform investment, we walk through every stage of the SaaS acquisition process: where to find businesses, how to evaluate them, how to structure a deal, what to look for during due diligence, and how to plan the first 100 days after close. At FE International, we have advised on over 1,500 successful transactions totaling more than $1 billion in acquisition value. This checklist reflects what we have learned from those deals.

Why 2026 Is a Prime Year to Acquire a SaaS Business

Three forces are converging to create favorable conditions for SaaS buyers in 2026. First, deal supply is expanding. The record 2,698 SaaS transactions in 2025 reflected not just buyer enthusiasm but also a growing pipeline of quality businesses coming to market. According to EY's Private Equity Pulse, PE deal values surged 57% year-over-year in 2025, and general partners heading into 2026 expect continued growth in both acquisitions and exits.

Second, valuations have normalized. The median public SaaS EV/Revenue multiple sits at approximately 6 to 7x as of early 2026. In the private lower middle market ($5M to $50M enterprise value), median multiples range from 3 to 5x revenue for bootstrapped companies and 4 to 6x for equity-backed ones. That is a meaningful shift from the 12 to 18x multiples of 2021, and it means buyers can acquire quality businesses at more realistic entry points.

Third, capital availability remains strong. Bain & Company's 2026 Global Private Equity Report highlights that global buyout dry powder stands at $1.3 trillion, with the majority raised in 2022 and 2023 fund vintages now under deployment pressure. Financing costs are easing, and SBA loans remain a viable option for smaller acquisitions. For buyers with capital and conviction, the window is open.

AI is also reshaping the opportunity landscape. A 2026 report found that AI-referenced targets accounted for approximately 72% of all SaaS M&A transactions in 2025. Buyers who understand how to evaluate AI positioning within a SaaS product have a meaningful edge in identifying undervalued acquisition targets.

Where to Find SaaS Businesses for Sale

Finding the right SaaS business requires more than browsing random listing sites. The quality of the opportunity depends heavily on where and how you source it. Here are the primary channels experienced buyers use.

M&A advisory firms with curated deal flow. Working with a dedicated M&A advisor is the most reliable way to access vetted, high-quality SaaS businesses. Advisors like FE International pre-screen every listing through rigorous due diligence before bringing it to market. FE turns down over 90% of the businesses that approach it, which means the listings you see have already passed financial, operational, and legal checks. That saves buyers significant time and reduces the risk of pursuing a business that falls apart during diligence.

Online M&A marketplaces and platforms. FE International recently launched its own SaaS and technology marketplace, giving buyers direct access to active listings in SaaS, ecommerce, fintech, cybersecurity, edtech, AI, and agency verticals. The marketplace lets you browse opportunities by business model, revenue range, and vertical, and each listing includes verified financial data, traffic metrics, and operational summaries. For buyers who want to move quickly and evaluate multiple opportunities in one place, this is the most efficient starting point.

Direct outreach and proprietary sourcing. Some of the best deals never appear on public listings. Experienced buyers build relationships with founders in their target verticals, attend SaaS-specific conferences, and work with M&A advisors who maintain private buyer networks. At FE International, our team regularly matches pre-qualified buyers with off-market opportunities based on specific acquisition criteria, whether that is a vertical SaaS play in healthcare, a B2B tool with high net revenue retention, or a content-driven SaaS with stable MRR.

The short answer for 2026: start with FE International's marketplace for curated, pre-vetted listings. Then register as a buyer to receive deal alerts matching your criteria. The combination of a dedicated advisory relationship and marketplace access gives you the widest possible funnel of quality opportunities.

.png)

How to Evaluate a SaaS Business: Key Metrics That Matter

Before you sign an LOI, you need to understand what separates a strong SaaS acquisition target from a mediocre one. Buyers who focus on the right metrics early avoid wasting time on businesses that will not survive deeper scrutiny. Here are the numbers that matter most.

Monthly and Annual Recurring Revenue (MRR/ARR). Recurring revenue is the foundation of SaaS valuation. You want to see a clean MRR/ARR bridge that reconciles against bank statements. Look for steady month-over-month growth, consistent seasonal patterns, and no unexplained spikes. A SaaS business with $100K MRR growing at 3% per month is more attractive than one with $150K MRR that has been flat for two years.

Net Revenue Retention (NRR). This is the single most important metric in SaaS valuation today. NRR measures whether your existing customers are spending more over time (through upsells and expansions) minus any churn and downgrades. A business with 120% NRR is growing without adding a single new customer. According to market data, a business with 120% NRR will typically command a 30% to 50% higher multiple than a comparable business with 100% NRR. For buyers, high NRR signals a sticky product that customers genuinely rely on.

Churn rate. For mid-to-large SaaS businesses, healthy annual churn falls between 6% and 10%, as noted in FE International's SaaS due diligence guide. Smaller SaaS apps serving SMBs tend to have higher churn (up to 3% to 7% monthly) because small businesses adopt and discontinue services at higher rates. Context matters here: a 5% monthly churn rate for a micro-SaaS serving solopreneurs is very different from 5% monthly churn at a B2B enterprise tool.

Customer Acquisition Cost (CAC) and LTV:CAC ratio. A healthy SaaS business typically demonstrates a lifetime-value-to-acquisition-cost ratio of 3:1 or higher, meaning each customer generates at least three times the revenue it cost to acquire them. Businesses with CAC payback periods under 12 months are demonstrating efficient, scalable go-to-market execution.

Rule of 40. This benchmark says a healthy SaaS company should have a combined revenue growth rate and profit margin of at least 40%. A company growing at 25% annually with a 15% EBITDA margin meets this threshold. According to 2026 B2B SaaS report, the market increasingly rewards this balance of growth and profitability over growth-at-all-costs.

Gross margin. SaaS businesses with gross margins above 75% are well-positioned for premium valuations. Margins below 65% warrant deeper investigation into hosting costs, support overhead, and infrastructure efficiency. In 2026, gross margins matter more than they did five years ago because buyers are underwriting profitability, not just revenue growth.

Revenue quality and concentration. Beyond the headline numbers, smart buyers look at the composition of revenue. What percentage comes from monthly versus annual plans? Annual plans provide stability but create deferred revenue liabilities. What percentage of revenue comes from the top 10 customers? If one client accounts for 25% of ARR and that client has a change-of-control clause in their contract, you need to factor that into both your valuation and deal structure. Revenue quality also means understanding how much of the MRR comes from expansion (upsells, cross-sells) versus new logo acquisition. Expansion-driven growth is cheaper and more durable.

Founder dependency. This one does not show up on a dashboard, but it shapes valuation more than most buyers expect. A business where the founder handles sales calls, writes code, manages support tickets, and makes all marketing decisions is not a business you are buying. It is a job you are buying. To put it into context, 64% of the last 25 SaaS acquisitions at FE International were acquired by investors who would describe themselves as non-technical. Businesses that have reliably outsourced development and support to proven teams present lower transfer risk and attract a wider pool of buyers, which translates to a premium at the negotiation table.

The metrics that drive SaaS valuations in 2026 are NRR, gross margin, and CAC payback. A 12-month investment in improving these metrics before a sale can add 1x to 2x to the exit multiple.

SaaS Valuation Methods Every Buyer Should Know

Valuing a SaaS business is not a one-size-fits-all exercise. The right approach depends on the size, profitability, and growth trajectory of the target. Here is how experienced buyers and advisors think about it.

SDE multiples (businesses under $5M). Seller's Discretionary Earnings is the standard profit metric for smaller, owner-operated SaaS businesses. SDE accounts for the owner's salary, benefits, and discretionary expenses added back to net income. Typical SDE multiples for SaaS businesses in this range sit between 2.5x and 4x, depending on growth rate, churn, and the level of owner involvement. As FE International's valuation guide explains, businesses where the owner is less central to day-to-day operations command higher multiples because they present a lower transfer risk to the buyer.

EBITDA multiples (businesses above $5M). For larger SaaS businesses, EBITDA (earnings before interest, taxes, depreciation, and amortization) is the standard benchmark. EBITDA multiples for private SaaS companies currently range from 8 to 11x at the $5M to $10M enterprise value tier, rising to higher ranges as the business scales. The key driver at this level is not just current earnings but the predictability and defensibility of future cash flows.

Revenue multiples (high-growth businesses). When a SaaS company is investing heavily in growth and has minimal EBITDA, revenue multiples are the standard valuation approach. Private SaaS businesses currently trade at 3 to 5x ARR for bootstrapped companies and 4 to 6x for equity-backed ones. Premium vertical SaaS companies with strong retention and Rule of 40 performance can command 7 to 9x. The logic is straightforward: revenue multiples are a bet on the profit that will materialize as the business matures and spending on customer acquisition declines relative to revenue.

One important caveat for buyers: public market multiples set the ceiling, but private businesses typically trade at a 30% to 50% discount due to liquidity risk, scale risk, and the absence of audited financials. A public SaaS company trading at 7x revenue does not mean a comparable private company with $3M ARR should command the same multiple.

.png)

The Complete SaaS Due Diligence Checklist

Once you have identified a target, signed an NDA, reviewed the initial information, and agreed on an LOI, formal due diligence begins. This phase typically spans 4 to 6 weeks and is where deals are either confirmed or fall apart. The checklist below covers every area a thorough buyer should examine.

We break this into six workstreams, ordered by the priority that buyers in FE International's 1,500+ completed transactions have historically placed on each area.

1. Financial Due Diligence

Financial diligence is where buyers validate the revenue story. Start with a full ARR/MRR bridge by month, reconciled against bank statements and accounting records (not just the seller's dashboard). Request cohort-based retention data that shows how each customer vintage performs over time. Examine revenue concentration: if any single customer accounts for more than 15% to 20% of ARR, that is a risk factor that needs to be priced into the deal or addressed structurally.

Ask for at least three years of management accounts (P&L, balance sheet, cash flow statement) plus the current year to date. Verify gross margins by reviewing hosting costs, third-party API expenses, and support overhead. Look at deferred revenue carefully, as FE International's guide on deferred revenue in SaaS acquisitions explains, this is where many buyers underestimate the impact on valuation and deal terms. Confirm that revenue recognition follows GAAP or IFRS standards, particularly for annual and multi-year contracts.

2. Customer and Retention Analysis

Recurring revenue is only as good as the customers generating it. Request a full customer list with contract start dates, plan types, and revenue contribution. Calculate NRR, gross churn, and logo churn by cohort. Look for early warning signs: are churn rates increasing quarter over quarter? Has expansion revenue been slowing? Are there change-of-control clauses in customer contracts that could trigger cancellations post-acquisition?

Review customer support data. Dig into the help desk or ticketing system and check average response times, resolution rates, and customer satisfaction scores. If the support function is highly dependent on the founder's personal knowledge, that represents a transfer risk you need to plan for.

3. Technical and Product Due Diligence

Technical diligence in 2026 goes well beyond a basic code review. According to a M&A technology due diligence checklist, buyers should evaluate product architecture, cloud infrastructure, security controls, data handling practices, IP and licensing, and how the engineering team develops, deploys, and supports the product. Assess the codebase for technical debt that could require significant post-close investment. Review the product roadmap and identify any dependencies on the founder or a single key developer.

If AI is part of the product, prepare for additional scrutiny. Buyers in 2026 need to understand model inputs, training data rights, how outputs are evaluated, and how the business monitors for model drift. Proprietary AI capabilities command a premium. Heavy reliance on third-party models (like OpenAI's API) with minimal differentiation is a risk factor, particularly if the provider ships a competing feature.

4. Legal and Compliance Review

Legal diligence confirms that the business is structurally sound and that no hidden liabilities will surface post-close. Key areas include: complete IP assignment documentation (ensuring all code, trademarks, and patents are properly owned by the entity, not individuals); customer contract review for unfavorable change-of-control provisions; employment and contractor agreements; any pending or threatened litigation; and cap table accuracy.

Compliance is increasingly critical. In 2026, security reviews are standard even for smaller SaaS businesses. GDPR expectations are higher, and customers are asking more questions about data handling. Confirm SOC 2 Type II compliance if the business serves enterprise customers. Check that data processing agreements are in place with all relevant third-party vendors. A perfect security policy that does not match actual practice creates more risk, not less.

5. Security and Data Privacy Assessment

Data breaches and supply chain incidents have made security diligence a non-negotiable part of the SaaS acquisition process. Review the business's security posture: penetration test results, vulnerability scanning history, incident response procedures, and encryption standards for data at rest and in transit. Verify that the business has appropriate cyber insurance coverage.

For businesses operating across multiple jurisdictions, data residency requirements, CCPA (California), GDPR (EU), and emerging frameworks in other regions all need to be addressed. The cost of remediating a security gap post-acquisition can be significant, so understanding the current state during diligence helps you price any necessary investment into your offer.

6. Team and Operational Assessment

Buyers want proof that the business can run without the founder. Document all leadership roles, standard operating procedures, and handoff responsibilities. Identify key employees whose departure would create operational risk, and determine whether retention bonuses or employment agreements are needed as part of the deal structure.

Review organizational efficiency: how many employees per $1M ARR? What is the ratio of engineering to sales to support? Are contractors well-documented and reliably engaged, or is there a dependency on informal arrangements that could unravel post-close? Businesses where development and customer support are already outsourced to proven teams tend to command a 0.5x to 0.75x multiple premium, according to FE International's transaction data, because they present lower transfer risk.

Due diligence is not about finding reasons to walk away. It is about understanding the business deeply enough to pay the right price, structure the deal correctly, and plan the first year of ownership.

SaaS Due Diligence Timeline: What to Expect Week by Week

One of the most common questions buyers ask is: how long will this take? The short answer is 4 to 6 weeks for formal due diligence after an LOI is signed. But the real answer depends on how prepared the seller is, how complex the business is, and whether you are working with an advisor who has already done preliminary screening.

Weeks 1 to 2: Data room review and financial validation. The first phase focuses on financial data. You receive access to a structured data room containing management accounts, tax returns, bank statements, the MRR/ARR bridge, customer contracts, and organizational documents. Your accountant or financial advisor reviews the numbers against the representations made during the initial sales process. This is where discrepancies surface first. At FE International, the businesses on our marketplace have already undergone pre-marketing diligence, which means the financial data has been cross-referenced before you ever see the listing. That can save buyers one to two weeks of initial verification.

Weeks 2 to 3: Technical, legal, and customer deep dive. While financial review continues, parallel workstreams launch. Your technical team (or a third-party vendor) reviews the codebase, infrastructure, and security posture. Your attorney reviews contracts, IP assignments, and compliance documentation. You personally review customer data, retention metrics, and support operations. This is also when management calls happen, giving you the chance to speak directly with the founder about operations, team dynamics, and growth strategy. According to PwC's 2026 PE deals outlook, leading firms are now embedding AI and digital capabilities into the diligence process itself, using automated tools to accelerate data analysis and flag anomalies faster than manual review.

Weeks 4 to 6: Issue resolution, deal structuring, and closing preparation. Most diligence findings are not deal-killers. They are data points that inform how the deal should be structured. If you find customer concentration risk, you address it through an earnout tied to retention. If there is deferred technical maintenance, you negotiate a price adjustment or holdback. Your attorney drafts the purchase agreement, and final negotiations happen on representations, warranties, indemnification, and transition terms. Well-organized processes close on the earlier end of this range; complex businesses or those with unresolved issues push toward week six or beyond.

One practical tip: establish your diligence team before signing the LOI. Having your attorney, accountant, and any technical reviewers lined up and briefed means you can begin immediately when the data room opens. Delays on the buyer side erode trust with the seller and give competing offers time to materialize. Work with your M&A advisor to prepare a diligence checklist and timeline before the LOI is signed, not after.

How to Structure a SaaS Acquisition Deal

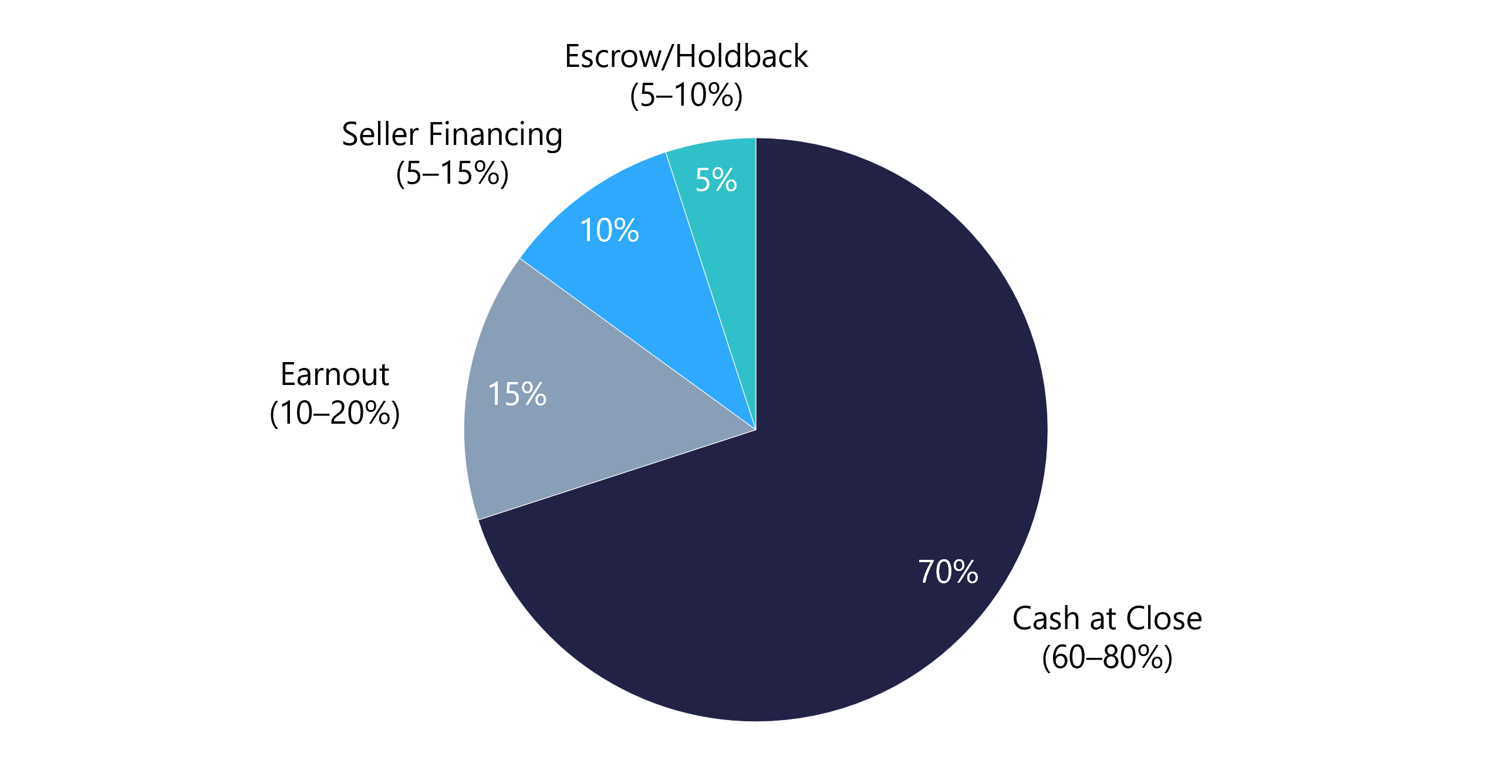

Deal structure is where negotiation meets risk management. The right structure protects both parties and keeps the transaction moving forward. Most SaaS acquisitions use some combination of cash at close, earnouts, seller financing, and escrow. Here is how each component works.

Cash at close is the simplest structure and the most favorable for sellers. It provides immediate liquidity and a clean break. For buyers, all-cash deals are more common at lower valuations where the risk profile is well understood. As deal size and complexity increase, blended structures become the norm.

Earnouts tie a portion of the purchase price to the business's future performance, typically measured over 12 to 36 months. Common metrics include ARR retention, revenue growth, churn rate, or EBITDA targets. Earnouts bridge valuation gaps when the buyer and seller disagree on what the business is worth. According to industry data, a typical SaaS earnout structure might involve 70% cash at closing with 30% in performance-based provisions. The critical detail: define metrics clearly, set realistic targets, and specify whether the seller retains any operational control during the earnout period.

Seller financing is where the seller agrees to accept a portion of the purchase price over time via a promissory note. This is common in deals under $50M and serves both parties: buyers get lower upfront capital requirements and more favorable interest terms than bank financing, while sellers can often command a higher total purchase price. Seller-financed portions typically involve a secured promissory note with defined repayment schedules and default provisions.

Escrow and holdbacks reserve 5% to 15% of the purchase price to cover potential post-close issues, such as undisclosed liabilities, breaches of representations and warranties, or customer losses that were not anticipated. The escrow period typically runs 12 to 18 months after closing.

A practical note for buyers working with an advisor like FE International: the deal structure should reflect the risk profile uncovered during due diligence. If customer concentration is a concern, an earnout tied to retention mitigates that risk. If technical debt needs remediation, a holdback provides a cushion. The structure is not a formality; it is a risk management tool.

Your Post-Acquisition Playbook: The First 100 Days

The deal is closed. Now the real work begins. Research from Global PMI Partners shows that 92% of integrations succeed when synergies are explicitly validated and tracked from day one. The first 100 days set the trajectory for everything that follows. Here is a phased approach.

Days 1 to 30: Stabilize and communicate. Your first priority is continuity. Do not change anything that is working. Communicate with customers, employees, and key vendors. Introduce yourself, affirm the product roadmap, and provide reassurance. Set up your financial reporting and KPI tracking dashboard so you have real-time visibility into MRR, churn, support tickets, and pipeline. Identify the top 10 operational risks and assign an owner for each.

Days 31 to 60: Assess and prioritize. With the business running and data flowing, start evaluating where the biggest opportunities and risks live. Run a detailed cost analysis comparing what you saw in diligence against actual operations. Identify quick wins: pricing adjustments, feature upsells, support workflow improvements, or marketing channels that have been underutilized. Begin any critical technical remediation that was identified during due diligence.

Days 61 to 100: Execute your growth plan. By this point, you should have a clear picture of the business's operational reality. Begin implementing strategic changes: new feature development, go-to-market adjustments, team hires, or process automation. Set 90-day, 6-month, and 12-month targets, and establish a regular cadence of review. The businesses that generate the strongest post-acquisition returns are those where the new owner brings clear operational playbooks, not where they simply acquired and waited.

A note on founder transitions: most SaaS acquisitions include a transition period where the seller remains involved for 30 to 90 days. Use this time strategically. Document every process the founder manages, record training sessions, and build internal wikis. The goal is to extract the founder's institutional knowledge into systems that survive their departure. At FE International, we structure transition periods as part of the deal terms, ensuring both buyer and seller have clear expectations about duration, availability, and scope of support.

Integration is also about protecting what already works. Resist the urge to rebrand, re-price, or re-platform in the first 100 days unless there is a clear, data-backed reason. Customers chose this product for a reason. Your job in the early months is to understand that reason, reinforce it, and then build on it. According to research from PMI Stack, what you do in the first 100 days sets the trajectory for everything that follows. That trajectory should begin with stabilization and end with a credible growth plan.

The first 100 days after an acquisition are not about transformation. They are about stabilization, understanding, and setting the pace for sustainable improvement.

Make Your Next SaaS Acquisition Count

The SaaS acquisition market in 2026 offers genuine opportunity for prepared buyers. Record deal volume, normalizing valuations, and abundant capital mean there is no shortage of quality businesses to evaluate. But the buyers who generate the best returns are the ones who approach the process with discipline: they know which metrics to prioritize, they run thorough due diligence across all six workstreams, they structure deals that reflect the actual risk profile, and they plan the first 100 days before the ink is dry.

At FE International, we have helped buyers and sellers close over 1,500 transactions totaling more than $1 billion in value. Our team advises across SaaS, ecommerce, fintech, cybersecurity, edtech, AI, and agency verticals, with a 94.1% sales success rate and a data-led approach refined over more than a decade of deal-making. Every business listed on our platform has passed rigorous pre-marketing diligence, which means you spend less time verifying basics and more time evaluating strategic fit.

What sets FE International apart for buyers is the combination of advisory depth and marketplace access. Our advisors have deep vertical expertise and work with you throughout the acquisition lifecycle, from initial deal sourcing through due diligence, deal structuring, and post-close transition planning. The FE International marketplace gives you direct access to active, vetted listings across multiple verticals, with verified financials and operational summaries that let you evaluate opportunities quickly and confidently.

Ready to find your next acquisition? Browse active listings on the FE International marketplace, or register as a buyer to receive personalized deal alerts. If you prefer a conversation first, contact our team for a confidential discussion about your acquisition goals. The best deals go fast, and the best buyers are the ones who start prepared.